Three ways to give smarter during the High Holy Days

Published September 20, 2022

The High Holy Days are just around the corner. Some of my fondest childhood memories involve spending time with family, listening to the sounds of the Shofar, devouring apples dipped in honey and overloading on challah. As we get older, many of us begin to understand that this is also a time of self-reflection and soul-searching. During this sacred season, Jews around the world reflect on the major biblical principles, also known as the Three Pillars: Teshuvah (Repentance), Tefillah (Prayer) and Tzedaka (Righteous Giving).

While Tzedaka literally translates to “righteousness” or “justice”, most of us equate the third pillar to mean “charitable giving”. Whether you choose to satisfy your Tzedaka goals by volunteering time or donating money to the causes that are important you, this is an excellent opportunity to consider what your long-term giving strategies are. I’ll focus on the three most common strategies you can do now:

- One way to give is to donate cash directly to a charity. Whether it be giving cash, writing a check, or paying with a credit card, this method is more often used by people because it is the easy and immediate. Taxpayers who itemize deductions are allowed to deduct the total amount that they give to charity each year, with a limit equal to 60% of their adjusted gross income (AGI). Taxpayers are allowed to carry forward excess contributions into future tax years if they exceed the 60% limit. If you do not have enough deductions (including your annual gifting) to be able to itemize, you may consider “bunching” more than one year of donations into a single year and reducing the number of years that you contribute. However, you will need to give more with this strategy to see a larger cumulative tax benefit for the same amount of charitable giving.

- For many people, there are more tax-efficient ways to give than by donating cash. Perhaps you have investment accounts that have grown over time and now have large unrealized gains on securities that you’ve held for longer than one year. Giving appreciated stock allows you to donate (and deduct) its current market value while also eliminating capital gains taxes you might otherwise owe. And if you were going to support a cause anyway, this approach can be a tax-efficient way to divest highly appreciated stock or rebalance back to your target allocation.

- Another popular giving option is the qualified charitable distribution (QCD). A QCD is a non-taxable IRA distribution that people 70½ years of age or older can send directly to a qualified charity. While there is no charitable deduction received for making a QCD, the amount of the distribution is tax-free. This is a strategy that is particularly advantageous for those taxpayers who choose not to itemize deductions. However, QCDs can help itemizers and non-itemizers alike by helping to minimize AGI and modified adjusted gross income (MAGI), to which many other benefits (e.g., credits) and additional costs (e.g., Medicare premiums) are tied. Note that for the QCD to work as intended, the distribution must go directly from the IRA to the charity. If the distribution is sent to the account owner, who then writes a check to the charity, then the income is taxable and the gift is tax-deductible.

The Days of Awe are a time where we self-reflect on what we’ve been doing versus what we should be doing. This magical season provides us the occasion to celebrate the promise of a new year with family and friends. When we give our time and financial resources, we can begin to correct wrongs and redirect our activities to the betterment of our neighbors. It is also a Shanah Tovah!

At Buckingham, we understand that each family’s goals and situations are unique. We would welcome the opportunity to create a personalized giving plan that utilizes your monetary donations in the most meaningful and cost-effective way. You are always invited to schedule a quick conversation with our team.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®.

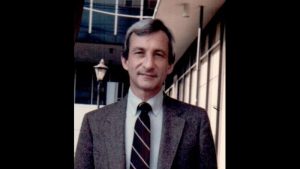

About the author:

John Corn has been a wealth advisor for Buckingham Strategic Wealth since 2004. He loves leveraging the collaborative environment at Buckingham to help his clients make smarter decisions and reach their financial goals. John also serves as a resource to other advisors and their clients regarding IRAs and general taxation. He has written various pieces for clients and advisors, including co-authoring a 2010 article on IRA conversions. John currently serves as a member of the Board of Trustees for Whitfield School as well as the Investment Committee for Congregation Shaare Emeth.